Short Answer

As you navigate through life’s milestones, have you ever stopped to ponder how much you should ideally have saved for retirement by a certain age? The prospect of retirement can seem distant, yet it looms large in the context of financial planning. Aiming for the top 10% in retirement savings can provide you with a comfortable cushion, allowing for a fulfilling, stress-free later stage of life. However, the challenge remains: Are you on track to meet these coveted benchmarks? Below, we delve into the retirement savings landscape delineated by age groups and elaborate on what it takes to achieve the top 10% of savers in the U.S.

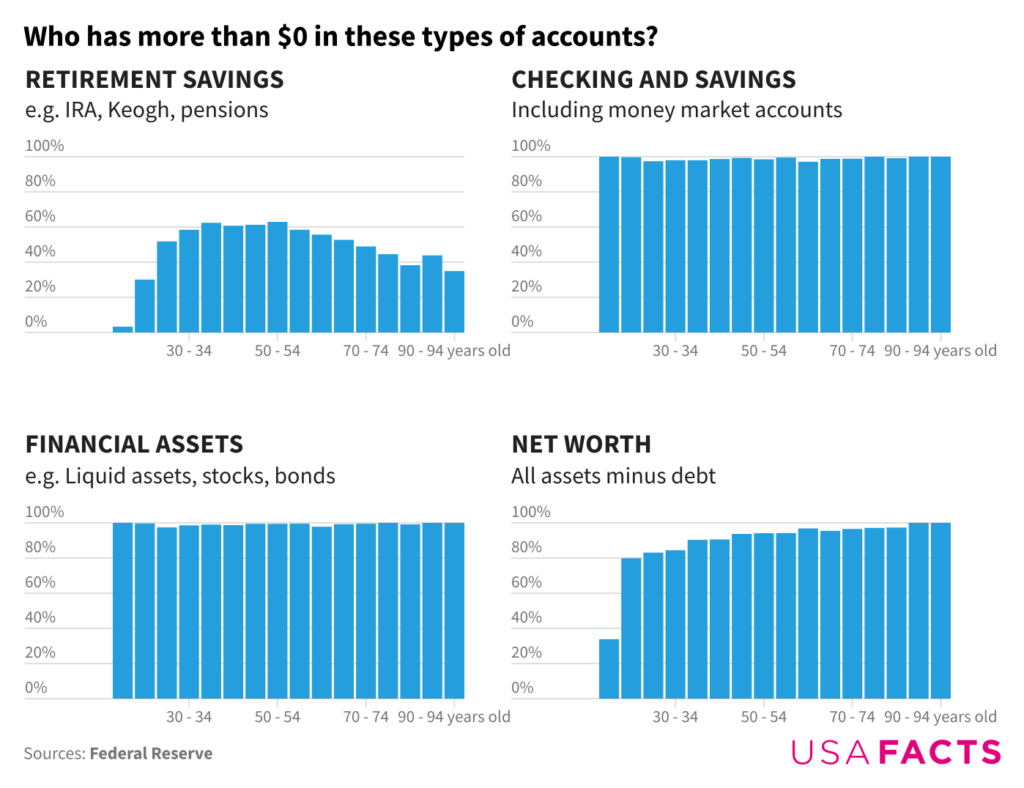

1. Ages 20-29: Early Beginnings

In your twenties, the world is brimming with possibilities, and retirement may be the last thing on your mind. However, the power of compound interest can be your ally if you start saving early. Aim for approximately $20,000 to be in the top 10% of savers by age 29. That means investing as little as $200 monthly, keeping in mind the long-term growth potential of your savings. Even in the early financial forays, consider diversifying your investments to bolster growth.

2. Ages 30-39: Building Momentum

Transitioning into your thirties, you may encounter significant life changes like marriage, home-buying, or expanding your family. During this decade, the ideal savings target is around $50,000 to maintain your standing among top savers. This figure demands a more concerted effort: a monthly contribution of about $450, based on annual investment growth rates. Embrace employer-sponsored retirement plans; contributing to a 401(k) can prove invaluable, especially if your employer offers matching contributions.

3. Ages 40-49: Acceleration Phase

As you reach your forties, financial responsibilities start to intensify. The median savings target by age 49 should be roughly $100,000 to parallel the top 10% of savers. During this period, you may wish to sharpen your financial strategy, focusing on maximizing contributions to retirement accounts. Diligently augmenting your savings rate to approximately $800 a month will bolster your retirement readiness. This is a time to become financially opportunistic, seeking growth in investments that align with your risk tolerance.

4. Ages 50-59: Nearing the Finish Line

Your fifties symbolize a crucial juncture. The baseline for elite savers hovers around $200,000 by age 59. This stage often welcomes the phenomenon of catch-up contributions, allowing those over 50 to contribute more to their retirement accounts. It is advisable to allocate around $1,500 monthly from now until retirement. This period can be paradoxical, filled with both excitement about nearing retirement and anxiety about achieving financial preparedness.

5. Ages 60-69: Retirement is on the Horizon

With retirements nearly within reach, in your sixties, the target can escalate to approximately $400,000 by age 69. By this time, it is paramount to possess a robust strategy for income generation and distribution. An influx of savings contributions—possibly $2,500 monthly—should be viewed through the lens of preserving wealth. It’s also the opportune time to assess your risk exposure amidst fluctuations in the market as you transition into retirement, striking the right balance between growth and preservation.

6. Ages 70+: Embracing Retirement

Once you cross the threshold into your seventies, the focus shifts from accumulation to preservation of wealth. By this age, achieving a target of $600,000 or more situates you among the most adept savers in the country. This number often requires mentoring from financial advisors to address complex issues such as longevity risk and healthcare costs. Your monthly distribution strategy must be well-planned to sustain an equable quality of life during your retirement years.

Countrywide Trends and Considerations

While the figures provided give a rough framework for retirement savings by age, it’s crucial to acknowledge that individual circumstances vary greatly. Factors like location, earning potential, and personal financial goals can significantly influence savings effectiveness. Keep in mind, within the U.S., the majority of adults in their forties and fifties often struggle to meet these benchmarks; therefore, the challenge resonates across demographics.

Additionally, as inflation continues to ebb and flow, the value of your retirement savings will undoubtedly fluctuate. While saving, consider the long-term implications of healthcare, housing, and potential unforeseen expenses that could arise. Consulting with financial experts can enrich your navigation through this financial labyrinth, ensuring a sustainable and prosperous retirement.

Conclusion

Ultimately, the journey towards reaching the top 10% of retirement savers is not only about the numbers. It is about developing a mindset geared towards future planning and disciplined saving. Engaging in regular reviews of your financial strategy can better equip you to either stay on course or recalibrate if necessary. As you reflect upon these guidelines and reflect on your own financial health, challenge yourself: Are you saving enough for the retirement you envision? The answers you yield could be transformative, paving the way to a fulfilling, well-equipped retirement life.

FAQ

What is the recommended retirement savings for people in their 30s?

For individuals aged 30-39, the recommended savings target to be in the top 10% of savers is approximately $50,000 with a suggested monthly contribution of about $450.

How can I catch up on retirement savings if I'm over 50?

People over 50 can make catch-up contributions to their retirement accounts, allowing them to contribute more than the standard limits to boost savings as they near retirement.

Why does retirement savings need to increase with age?

Increasing retirement savings targets with age accounts for the shorter time horizon to grow investments, rising expenses, and the need for a larger retirement fund to sustain longer post-retirement life.

How does inflation affect retirement savings?

Inflation reduces the purchasing power of saved money over time, making it important to consider inflation-adjusted returns and costs when planning for retirement.

Leave a Reply