Short Answer

In the vast and intricate tapestry of retirement planning, 401(k) accounts serve as a cornerstone for financial security in the golden years. As individuals journey through different life stages, the accumulation of wealth within these retirement vehicles can starkly vary. Understanding the highest 401(k) balances by age not only sheds light on successful financial habits but also provides a motivational framework for those aspiring to optimize their savings. This exploration promises to redefine perspectives on retirement strategy, offering insights that may very well inspire a shift in personal finance philosophies.

Below, we delve into the top 10 highest 401(k) balances categorized by age group. The information elucidates the trajectories of wealth accumulation, showcasing the nuances of saving that can lead to impressive nest eggs.

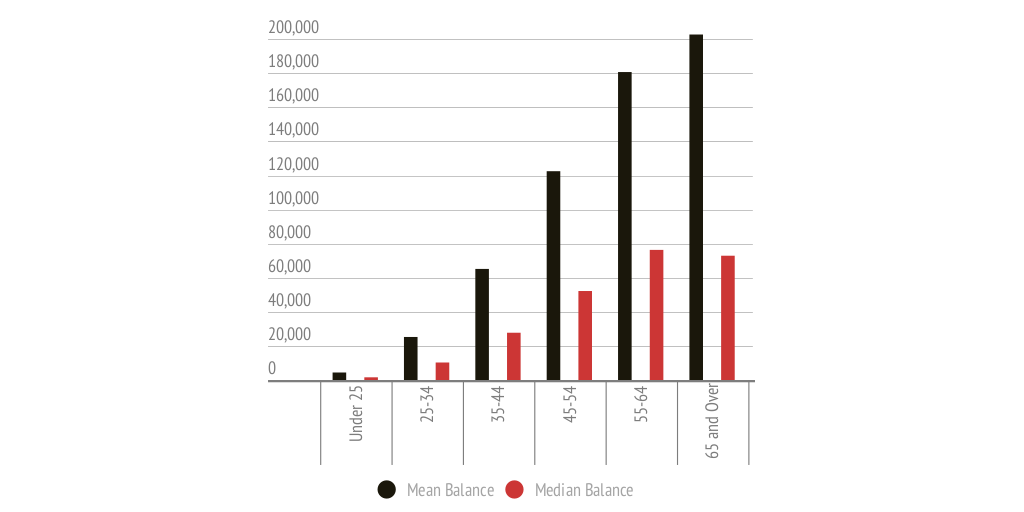

1. Ages 20-29: The Foundation of Futures

In the burgeoning arena of adulthood, individuals aged 20 to 29 often face a whirlwind of financial decisions. While the average 401(k) balance for this group hovers around a modest level, those who prioritize early contributions can exceed expectations significantly. Savvy savers in this age range often embrace the power of compound interest and employer matching, laying a robust foundation for their future. The most ambitious among them could see balances nearing $100,000, a daunting yet exhilarating possibility.

2. Ages 30-39: The Accumulation Surge

As this cohort embarks on significant life milestones such as homeownership and parenthood, financial strategies evolve dramatically. With a decade of earning experience under their belts, individuals aged 30 to 39 begin to accumulate wealth at a more pronounced rate. The highest balances in this demographic can soar to around $200,000. This age group often benefits from heightened salary increases and stronger investment acumen, with many adjusting their risk tolerance to capture higher returns.

3. Ages 40-49: The Peak of Progress

Entering the 40s, many savers start seeing the fruits of their earlier efforts solidifying into substantial 401(k) balances. Average savings around this age can easily eclipse $300,000 for those who diligently contribute and invest wisely. The highest achievers may reach balances of $500,000 or more, as they recognize the urgency of maximizing contributions during their peak earning years. With retirement looming closer on the horizon, strategic reallocations and diversified portfolios often characterize this age group.

4. Ages 50-59: The Catch-Up Catalyst

The 50s signify a crucial period for fortifying retirement plans, as individuals become eligible for catch-up contributions. This age bracket offers a unique opportunity where individuals can heighten their contributions, often resulting in dramatic increases in 401(k) balances. Those who invest astutely might amass upwards of $700,000. This phase emphasizes not just saving but strategic financial planning, balancing growth with security, to safeguard against potential market volatility.

5. Ages 60-69: The Golden Nest Egg

Approaching retirement, individuals aged 60 to 69 typically reflect on decades of hard work that culminate in substantial retirement savings. Average 401(k) balances in this group often average around $800,000. However, those who exercised financial prudence and made consistent contributions might exceed $1 million, positioning themselves well for retirement. As retirement becomes more imminent, the focus often shifts to capital preservation and income generation, ensuring their savings last through the decades ahead.

6. Ages 70 and Above: The Wealth Legacy

The journey through retirement is uniquely impactful for those aged 70 and above. While many may begin to draw on their accumulated wealth, some individuals maintain 401(k) balances that soar beyond $800,000, thanks to strategic investment choices, disciplined savings, and delayed withdrawals. This demographic not only serves as a testament to successful financial management but also underscores the importance of legacy planning, ensuring their wealth can be preserved and possibly passed on to future generations.

7. The Role of Employer Contributions

One cannot overlook the pivotal role that employer contributions play in maximizing 401(k) balances. Many organizations offer matching contributions, a powerful incentive that can significantly boost an employee’s total savings. It’s essential for individuals to take full advantage of these programs. Doing so effectively can be the difference between a comfortable retirement and financial strain.

8. Investment Strategy: Risk and Reward

Investment strategy serves as the backbone of 401(k) growth. A diversified portfolio tailored to one’s risk tolerance can exponentially increase balance growth. Younger savers are often encouraged to embrace a riskier investment approach, placing their funds in growth-oriented stocks, while those nearing retirement may pivot towards more stable options. Understanding the interplay of risk and return is crucial to crafting a financially sound future.

9. The Impact of Financial Education

Investing in financial education can set individuals apart in their retirement strategies. Knowledge of market dynamics, asset allocation, and retirement planning tools empowers individuals to make informed decisions. Those who proactively seek out educational resources often see higher balances as they are more likely to contribute consistently and invest wisely.

10. The Future of Retirement Savings

As economic landscapes evolve and longevity increases, the necessity for robust retirement planning becomes paramount. The trends in 401(k) balances reveal not only individual achievements but also society’s broader financial literacy and saving ethos. A commitment to continual education and adaptable strategies can redefine what is possible for future generations navigating their financial futures.

In conclusion, the journey through various life stages illuminates the transformative power of strategic saving and investment within 401(k) plans. By understanding the potential balances achievable by different age groups and the pivotal factors influencing them, individuals can glean valuable insights to shift their own financial perspectives. As the world of retirement planning continues to evolve, so too must the approaches individuals take to secure their financial futures, paving the way for a luscious landscape of financial empowerment.

FAQ

What are the highest 401(k) balances by age group?

The highest 401(k) balances typically increase with age, ranging from around $100,000 for individuals aged 20-29 to over $1 million for those aged 60-69.

How do employer contributions impact 401(k) savings?

Employer contributions, such as matching funds, significantly enhance 401(k) balances by supplementing employee contributions.

Why is it important to adjust investment strategies over time?

Adjusting investment strategies according to age and risk tolerance helps maximize growth in earlier years and protect accumulated savings as retirement nears.

What is the benefit of catch-up contributions?

Catch-up contributions allow individuals aged 50 and older to contribute more to their 401(k), helping to accelerate savings as retirement approaches.

How can financial education improve retirement outcomes?

Financial education equips individuals with knowledge to optimize contributions, choose appropriate investments, and plan effectively for retirement.

Leave a Reply