Short Answer

As the fiscal landscape evolves, understanding the tax obligations of the top 10% of earners in the United States remains a topic of heated discourse and curiosity. By 2026, projected changes in tax legislation and economic shifts are anticipated to significantly alter the financial responsibilities of this affluent demographic. This exploration delves into the intricate web of factors that shape these tax contributions, providing readers with a comprehensive breakdown that promises to shift perspectives on wealth and taxation.

1. The Socioeconomic Spectrum of Income

The phrase “top 10%” refers not merely to an arbitrary classification but encompasses a diverse array of income earners, exhibiting a wide range of professions, from CEOs and entrepreneurs to highly specialized professionals in fields such as finance and technology. The thresholds for this tier are continually adjusted, currently set around an annual income of about $200,000. However, in 2026, projections suggest this minimum requirement may be influenced by inflationary pressures, thereby expanding the demographic associated with this elite earning group.

2. Federal Tax Rates and Bracket Adjustments

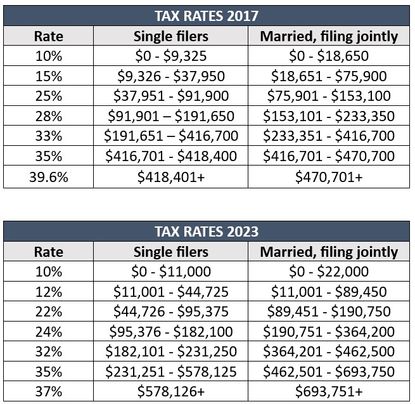

As we glance at the federal income tax rates, the top 10% is embroiled in a complex and evolving system. For the 2026 tax year, federal income tax brackets are expected to experience minimal revisions, maintaining the existing percentages but potentially recalibrating the bracket thresholds to reflect the rapid adjustments in cost of living. Anticipated rates for this income group may hover around the top tier of 37%, imposing a substantial burden on high earners, especially those with fluctuating incomes from investments or businesses.

3. Capital Gains Tax Considerations

Integral to the financial calculus of the upper echelon is the capital gains tax—particularly relevant for individuals whose wealth is predominantly derived from investments rather than wages. This category, which could witness a shift in treatment, demands meticulous attention. In 2026, expected modifications may include a potential increase in long-term capital gains tax rates, prompting affluent investors to strategize around tax loss harvesting and other fiscal maneuvers to mitigate tax liability. Such a change could either serve as a deterrent to speculative investments or bolster public revenue, thereby igniting debates regarding fairness and economic stimulation.

4. State and Local Tax Implications

Beyond federal obligations, state and local taxes constitute a critical component of the overall tax burden. Different states have tailored their tax policies, resulting in a patchwork structure that varies dramatically—occasionally exceeding federal rates in certain high-tax jurisdictions such as California and New York. An increasing number of states are contemplating reforming their tax codes to ensure higher earners contribute a proportionate share, thereby compelling the top 10% to navigate a labyrinth of taxation that further complicates their fiscal engagement.

5. The Impact of Deductions and Credits

Throughout this intricate fiscal narrative, taxpayers within the top 10% often utilize various deductions and tax credits to curtail their taxable income. However, revisions in tax policy may affect the availability and efficacy of these benefits. The discussions surrounding the elimination of the cap on state and local tax (SALT) deductions indicate a trend towards increasing financial accountability among high earners. Evaluating how the loss of certain deductions could reshape the burden for the top 10% is paramount in understanding their overall tax strategy.

6. Wealth Tax Considerations

As public discourse increasingly gravitates towards wealth taxation, the implications for the top 10% become pronounced. Proposals to impose wealth taxes could revolutionize the landscape of taxation, potentially levying taxes on assets rather than solely on income. If such legislation comes to fruition by 2026, it would represent a fundamental shift, compelling those within this echelon to become more astute in asset management and retirement planning.

7. Philanthropic Obligations and Tax Benefits

Philanthropy naturally intertwines with financial strategies for high-income individuals. Charitable giving not only serves societal purposes but can also function as a conduit for tax relief. In 2026, as tax policies evolve, philanthropic initiatives may see a corresponding increase due to favorable tax treatments designed to stimulate greater giving. This reciprocal relationship between altruism and taxation raises significant questions: What could be the long-term ramifications for societal equity and reliance on private funding for public goods?

8. The Role of Corporate Taxes

Many individuals among the top 10% either lead corporations or derive income from them. Changes in corporate tax rates, combined with regulations on retained earnings and distribution strategies, have direct consequences for personal tax responsibilities. Understanding how these shifts can create ripple effects in individual tax liabilities is crucial for a holistic understanding of the top earners’ contributions to public revenue.

9. Global Comparisons and Tax Competition

The discussion of tax obligations cannot occur in isolation; it must encompass a global perspective. As various countries contend for economic supremacy, the competitive nature of taxation takes center stage. Should the U.S. maintain or pivot its tax structure, the resulting implications for high earners could compound as they leverage international avenues to minimize tax burdens, potentially siphoning critical revenue away from domestic coffers.

10. The Future of Taxation for the Affluent

As 2026 approaches, the interplay of legislative reform, economic dynamics, and public sentiment will undoubtedly redefine tax contributions for the top 10% of earners. This evolving narrative will necessitate a sophisticated understanding of financial mechanisms, societal obligations, and the broader implications for wealth distribution. The journey into the complexities of taxation invites reflection on the moral and ethical dimensions of affluence and accountability in an increasingly interconnected world.

In conclusion, the intricate tapestry of taxes paid by the top 10% in 2026 beckons further examination and discussion. Through understanding the multifaceted implications of these various factors, individuals, policymakers, and society at large can engage in constructive dialogues about fairness, responsibility, and economic stewardship.

FAQ

What is the definition of the top 10% income earners?

The top 10% income earners are typically those making over $200,000 annually, though this threshold is projected to change with inflation by 2026.

How might federal tax brackets change in 2026?

Federal tax brackets may see minimal percentage changes but could have threshold adjustments to keep pace with inflation.

What changes are expected in capital gains taxes for high earners?

There may be an increase in long-term capital gains tax rates, encouraging tax planning strategies among investors.

How do state taxes affect the overall tax burden for the top 10%?

State and local taxes vary greatly, with some states imposing rates higher than federal taxes, complicating the total tax liability.

What is the potential impact of a wealth tax on top earners?

A wealth tax would levy taxes on assets, not just income, potentially increasing financial obligations for the affluent.

Leave a Reply